Defying expectations, spot rates stay elevated

Spot rates on DAT MembersEdge stayed elevated on most high-volume lanes last week despite a slight decline in volumes and a modest bump in capacity compared to the previous week. It’s an unusual pattern as volumes tend to diminish and capacity typically loosens from now through to early October.

Nationally, the number of available loads dipped 1.5% last week while truck posts increased 1.3%.

National average spot rates, July (rolling average including fuel)

- Van: $2.02 per mile, 21 cents compared to June.

- Flatbed: $2.18 per mile, up 11 cents.

- Reefer: $2.29 per mile, up 14 cents.

These are rolling averages through July 19 and include a fuel surcharge. Line-haul rates (the spot rate excluding a fuel surcharge) averaged $1.82 for vans, $1.94 for flatbeds, and $2.07 for reefers.

Trends to watch

Imbalanced freight networks

Contract and spot rates have not moved in sync as they normally do. Spot rates as of last week have risen faster since May and are now close to contract rates for all three major equipment types. This is a direct result of the ongoing COVID-19 pandemic, which points to more inconsistent freight volumes and unbalanced carrier networks in the short-term as shippers send more loads to the spot market to meet erratic demand and carriers increasingly become more selective about the contract loads they haul.

Retail van freight volumes

Average spot van rates were higher on 65 of DAT’s top 100 lanes by volume last week compared to the previous week while the volume of loads increased on 90 lanes. Pricing edged higher in several key retail freight hubs compared to the previous week:

- Allentown, Pa.: $2.36 per mile, up 16 cents.

- Los Angeles: $2.84, up 8 cents.

- Memphis: $2.48, up 8 cents on a 35% increase in load volumes.

- Houston: $1.94, up 3 cents.

Some examples of where prices are still rising last week:

- Dallas to Memphis, Tenn., jumped up 14% at an average of $1.85 per mile.

- Chicago to Buffalo, N.Y., was up 29 cents to $2.92.

Southern California vans

Los Angeles and Ontario, Calif. – key hubs for import traffic – saw a 19% drop in load posts from the peak on June 27 and are now back to seasonal levels. Just over 15% of Los Angeles and Ontario-outbound loads last week were destined for the major warehouse markets of Stockton and Phoenix, which is consistent with the staging of imports for back-to-school retail season.

Seasonal reefer spot rates

Average spot rates last week were higher on 33 of DAT’s top 72 reefer lanes by volume compared to the previous week. Nineteen lanes were neutral.

Produce shipments

Reefer volumes on DAT’s top 72 lanes last week declined for the fourth consecutive week. The U.S. Department of Agriculture reported that seasonal truckloads of domestic produce fell 8% and imported produce fell 3%. That’s the equivalent of 4,868 fewer loads than the prior week. Produce volumes from Mexico continue to fall from their mid-June high, but are down 6% year over year due to decreased demand in the U.S. foodservice sector. Load volumes from the California produce markets of Fresno, Ontario, Stockton and San Francisco increased 9% week over week and are now up 28% over the last three weeks.

Reefer freight out of the Pacific Northwest is being driven by pears, cherries, apricots and potatoes, which is pushing demand out of Spokane, Wash.; Medford, Ore.; and Twin Falls, Idaho.

Flatbed volumes mixed

Flatbed load volumes were mixed last week, with 37 of the top 78 flatbed lanes trending higher compared to the previous week.

Volumes in the Southeast remain strong, however, especially from Alabama, Texas, Arkansas, Georgia, and Mississippi. Load posts last week out of the region topped 211,000, which represents a 17% week over week and 31% month over month increase. Spot rates are also up 15% over the last three weeks. In Texas, Fort Worth and Lubbock were hot markets for available trucks. The average rate on 58 origin-destination pairings increased from $1.90 to $2.09 per mile, with shorter, regional moves to Shreveport, La., and Little Rock, Ark., paying $3.23 and $2.94 respectively.

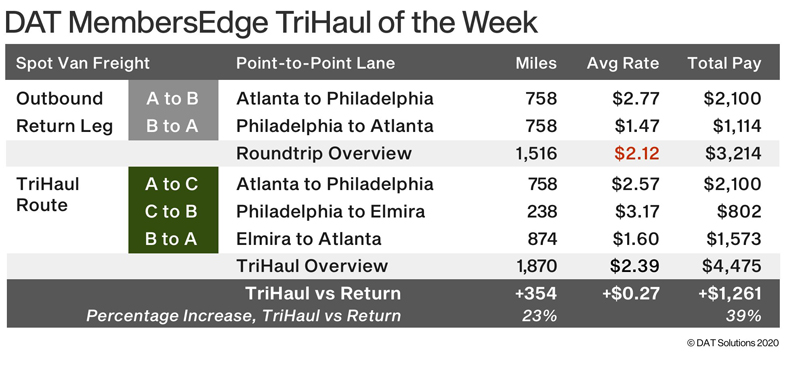

Tri-haul of the week

Spot van freight from Atlanta to Philadelphia averaged $2.77 a mile last week but the return was just $1.47, a fairly typical spread between the two directions. With higher spot rates on other lanes out of Philly, use the tri-haul tool in DAT MembersEdge to find a better-paying alternative back to Atlanta.

The top suggestion right now: Philadelphia to Elmira, N.Y., a key manufacturing area in upstate New York.

Philly to Elmira averaged $3.37 last week, and the lane from Elmira back down to Atlanta averaged $1.80. This tri-haul does add about 350 miles to the total trip, not counting any deadhead between drop-offs and pickups, but even if you just negotiate the average rate on the three loads, the rate per loaded mile jumps up 27 cents compared to the normal roundtrip. That works out to more than $1,200 in added revenue if you can make it work with your schedule.

Remember, these rates represent averages from last week, and this week will be different. Negotiate the best deal you can get on every haul, and look at the rates and load-to-truck ratios in MembersEdge to understand which way the rates are trending.

For the latest spot market updates related to COVID-19, visit DAT.com/industry-trends/covid-19 and follow @LoadBoards on Twitter. You can post comments on the DAT Freight Talk blog or on the DAT Facebook page. You can listen to the DAT MembersEdge report every Wednesday on Land Line Now.

Here’s the DAT report from late June.

Related News